08-07-2026

08-07-2026

|

Getting your Trinity Audio player ready...

|

This post originally appeared on the ZeMing M. Gao’s website, and we republished with permission from the author. Read the full piece here.

This is the most significant Bitcoin chart to look at, because it is signaling the future.

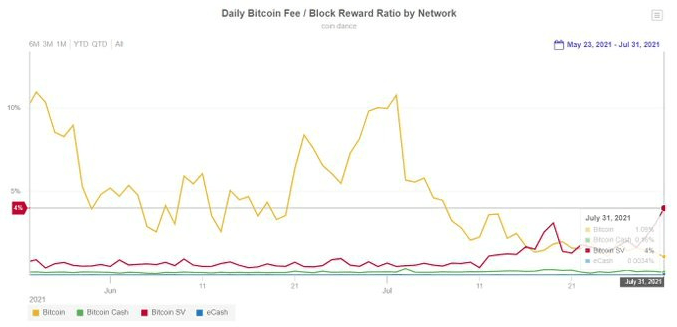

BSV’s transaction fee to total block reward ratio has surpassed that of BTC on July 16, 2021, for the first time, and seems to be opening up a runaway gap, standing at 4x over BTC as of August 1, 2021. (Source: coin.dance. The chart shows daily ratios, but the ratios computed block to block averages would essentially be the same.)

Why is this important? Because this is where the dynamics of competitive mining economics lies. And if the trend continues, BSV miners will enjoy exponential growth of revenue from network fees, while BTC miners will face growing avalanche pressure to migrate to BSV for superior profitability, and this is despite the fact that fee per transaction on BSV is many thousands times lower than that on BTC and is likely to continue to drop further lower by many times in the future.

At the most basic level, the economics of Bitcoin mining is not complicated, and is the same with BTC as with BSV.

Miner’s block reward = block subsidy + network transaction fees

The block reward is a miner’s revenue for successfully creating a valid block on the chain.

As will be shown in this article, in terms of comparative mining profitability, the block subsidy parts essentially cancel out on each other among BTC, BSV and BCH, and therefore the only competitive action is found in the network transaction fees.

And as will be shown in this article, the trend of the network transaction fees, along with the inherent designs of BTC and BSV, means bad news for BTC.

Please do not quickly jump into the following superficial conclusions:

- Because presently there is a huge price difference between BTC and BSV coins, the block subsidies are not comparable and cannot possibly cancel out on each other.

- Because historically the BTC’s fee percentage reached levels that were much higher than even the BSV’s recent highest fee percentage, the current trend must be a temporary fluke.

Your intuition is wrong if you think the above. Read on. But first a hint:

The actual prices of BTC and BSV are irrelevant in this analysis, since the dynamics is determined by the relative ratios, and the fundamental profitability metric is the profitability per-unit hash power (rather than that of the total hash power).

For example, currently, BSV price is 1/300th that of BTC. But as far as the mining subsidy only is concerned, mining on BSV is equally profitable to that on BTC, because mining BSV requires 300 times less hash power. Therefore, the subsidy part of the economics evens out between BTC and BSV, and the only thing that is competitive comes from the network transaction fees, which is a focus of this article. This is not a theory. If you’re a miner, whether you understand this intellectually or not, you will actually feel it in your mining operations. Anyone who has done multi-chain BTC/BCH/BSV mining simultaneously would know this as a fact.

The background & status quo

As said above, the block reward is a miner’s revenue for successfully creating a valid block on the chain.

And creating a valid block involves two major types of work performed by the miner, namely:

(1) building a block, and

(2) proving the block.

Building a block including adding and processing transactions in the block. It can be very simple when the miner includes only those transactions that have simple straight scripts, but may become very complex when the miner includes transactions that have complex smart contracts. For BTC, there is no smart contract. All transactions on BTC have simple standard scripts and a miner needs no special software nor technological know-how to process these transactions. With BSV, however, a new field is opened up because more and more transactions are created to take advantage of the smart contract capability on BSV. A BSV miner has a choice to make when building a block, namely deciding what transactions it wants to include in the block it is building.

This is where the BSV mining business becomes sophisticated and competitive beyond the mere hash power competition. A BSV miner cannot just blindly include every transaction into its block. Transactions having smart contracts can be highly complex, and they can come from all kinds of customers in various businesses, from art, esports to enterprise software. To include such a transaction in a block requires a good understanding of the customer’s business logic, building a good business relationship with the customer, and developing software capabilities to compile the smart contracts to straight OP_codes. Advanced miners may even go beyond and start to build tools for new businesses in BSV blockchain ecosystem. There is no limit.

Proving a block is a different matter. Broadly speaking, it involves two different kinds of block proving activities:

(i) solving a hashing puzzle, which is a hashing competition among miners for the next block (as every miner builds its own block and wants its block to be accepted in the chain), and

(ii) validating and accepting the block created by another miner who has won the hashing competition (miners are required to do this is matter of the consensus).

Note that the miner who has won the next block does not need to do extra work in validating and accepting the block, because all that should have been done already in building the block, see the above (1). But to be accepted to the chain, the block has to be validated and accepted by other miners.

It is important to also note that, after a block has already been built, validating and accepting the block by another miner becomes easy and can be done by any miner, because all have been compiled into straight scripts (OP_codes). In other words, although not every miner may be sophisticated enough to build a block to include transactions that have complex smart contracts, every miner that runs standard mining software is capable of validating and accepting such a block created by another miner.

Bitcoin protocol uses Proof-of-Work (PoW) to build a consensus among the miners.

The concept of PoW itself has been a source of confusion, because by “work” in Proof-of-Work, most people refer to “hashing” only. But that’s a misunderstanding, because there are at least two different types of work involved as indicated above.

The term “mining” is also confusing, because to many people, it suggests working for newly “minted” coins as a block subsidy only. But that is not accurate, because in reality:

(1) there is no ongoing “minting” (in a real sense of the term) of Bitcoin, as all 21 million bitcoins were minted all at once when the Genesis block was created; and

(2) the only difference between block subsidy and network transaction fees is that the former receives new coins from the preprogrammed coinbase (an initial market) while the latter receives coins from customers (a secondary market).

Therefore, even if the block subsidy has stopped, miners’ work will continue and may still be considered as being “mining” in a sense that the process yields coins for a miner.

It is therefore misleading to focus on the block subsidy only. Block subsidy is supposed to be a temporary bootstrapping strategy for establishing the blockchain, but the real dynamics of the mining economy is supposed to be in the network fees.

The block subsidy is mostly static (except for halvings roughly every four years). And more importantly, as will be shown in this article, block subsidies are non-differential between different chains (that is, they are essentially the same for BTC, BSV or BCH on unit-hash power basis).

Currently, BTC and BSV prices track almost precisely in proportion to the network hashing powers. In other words, the ratio between BTC price and BSV price is almost exactly the same as the ratio between BTC hash power and BSV hash power (which both stand close to 300:1 presently). Both ratios fluctuate with time, in the range of 200:1 to 300:1 in the recent year, but they are almost synchronized.

It means the market is completely writing off the network transaction economics.

This reflects a temporary fact that the fee percentages of both networks are still very low and almost negligible (i.e., the network transaction fee is still a small portion on these networks and have a negligible impact on miners’ decisions on operations).

However, this ignores what is already happening behind the scenes and will likely happen at an even faster pace in the future.

But watch the trend!

The network transaction fee is rapidly growing as a component of the BSV’s total block rewards, while the counterpart of BTC is perpetually limited by design.

Imagine when BSV’s fee percentage rises above 90%, while that of BTC remains at 1%. It would mean that for the same amount of hash power, a miner would generate 10 times (10x) as much revenue on BSV as that on BTC. And it would also translate to much higher profits (see Section “What about profitability?”).

And at 99%, it would be about 100 times, so on. See further below for a more detailed mathematical explanation for this conclusion, but at this point, just trust the math.

But in reality, that’s not going to happen, as miners would have moved over to BSV long ago. Who can ignore a 2x in profitability, let alone 10x?

BTC miners therefore face a growing avalanche pressure due to BSV’s exponential growth of network fees. If a 10% or 20% extra profit margin is not sufficient to overcome ignorance, ideological bias, personal sentiments, whatever the case it may be, how about 50%, 100%, 200%, 500%, or 1000%?

Wherever there is a higher profit to be made, the capital and resources will figure out a way to follow. It is simple economics and capitalism. A rapidly growing economic force cannot simply be ignored or pushed back by mere slandering. There will bound to be reactions, legally or not.

So overall, as long as the BSV adoption continues, it will all gravitate toward BSV.

For the same reason, the apps and transactions on BSV are absolutely the key. If they keep going up like they have been during the last month, something big is going to happen in the BSV landscape, including the coin price. It will not be a matter of personal opinions, but objective economics.

The present and the future

The present price difference between BTC and BSV is a known fact. The purpose of this article is to help readers focus on the trend.

It is important to realize that BTC’s network fees are limited by design and have already reached the upper limit, while BSV’s are unlimited. The potential room of growth is over a million times from here. This is a fact, not an opinion. Keep this in mind while reading this article to save me from repeating, as otherwise some of the logic and reasoning may not come through naturally.

That BTC’s daily fees has almost a hard cap is also a well-known fact. It is because the total number of transactions the BTC blockchain can process is already at its maximum block capability. Although the actual number fluctuates from time to time, it has touched the top frequently in the past. And by the very design of BTC which predicates on small blocks, the top is a hard ceiling, with no possibility to pierce through.

With the total number of transactions per block fixed, the only way to increase the transaction fee is to increase the fee per transaction, which is unrealistic because it is already above $10.

In contrast, BSV has unlimited block size, and therefore unlimited number of transactions per block. At the same time, the fee per transaction for BSV is less than one cent, and has room to go even lower due to competition. For more detail, see BTC and BSV, what is the real difference?

It really is an exciting time to be in the BSV space.

The dynamics between hash power and price

The dynamics between hash power and price is not a simple cause and effect relationship. Nevertheless, the correlation and even causality between hash power and price is real:

The total hash power of a blockchain (BTC or BSV) is largely determined by the block difficulty level. Block difficulty adjustment happens once a while due to the 10-minute block time restriction, which is affected by miner competition (because more competition leads to higher hash power and thus shortens block time), which, in turn is driven by miners’ profitability, which again, in turn, is determined by revenue sources and the coin price.

The coin price at any given time is determined by the market.

The market is influenced by demand and supply.

With an asset that has no utility, the demand and supply is mostly speculative, depending on people’s perception of the future price, the network strength (which in turn correlates to hash power), the selling of newly minted coins by miners, and many other things. It is therefore not a simple one directional linear relationship.

But as BSV processes more and more transactions, and bigger and bigger blocks, BSV becomes a real commodity, not for pure speculative trading, but actually needed by businesses, entrepreneurs, consumers to have transactions and to store data on the BSV chain.

Thus, a market that has real economic basis emerges, and BSV price will be driven by economic demand and supply, not just speculations.

As the demand increases, the price will increase too, because BSV has a limited supply.

Therefore, it emerges as a clear picture that, with more transactions and bigger blocks, BSV price has nowhere to go but to rise.

But if the BSV price continues to rise, BSV hash power will rise as well. Will the attraction for miners to move to BSV be reduced as the BSV price rises?

The answer is no, because ultimately, a miner’s acts such as willingness to increase its hash power are driven by profitability. This is science according to economics. Due to the extra transaction revenue, the mining economics keeps being in favor to BSV, because no matter how much BSV hash power rises, it cannot make the transaction revenue advantage of BSV mining disappear.

Definitions and examples

In order to look at this more quantitatively, let us look at several definitions.

- Block reward = block subsidy + network transaction fees

- BSV/BTC hash ratio: BSV hash power / BTC hash power

- BSV/BTC price ratio: BSV price / BTC price

- BSV’s fee percentage: BSV network fee / BSV block reward (%)

- BTC’s fee percentage: BTC network fee / BTC block reward (%)

- BSV-BTC fee percentage difference: BSV’s fee percentage minus BTC’s fee percentage (%)

So the issue before the miners is quite simple:

Anytime when BSV’s fee percentage is greater than BTC’s (that is, BSV-BTC fee percentage difference greater than zero), there is attraction/pressure for a miner to move its hash power from BTC to BSV, because the difference is almost free surplus profit, provided that the BSV/BTC hash ratio and BSV/BTC price ratio are the same (which has been the case historically).

This is because when BSV/BTC hash ratio and BSV/BTC price ratio are the same, the block subsidy alone results in the same profitability on BSV and BTC.

For example, currently, BSV price is 1/300th that of BTC, but if the mining subsidy only is concerned, mining on BSV is equally profitable to that on BTC because mining BSV requires 300 times less hash power (and correspondingly 300 times less equipment and energy). So the subsidy part of the economics evens out between BTC and BSV.

At the present time, because the fee percentages of BTC, BCH and BSV are all very small, the mining profitability of these three chains are essentially the same per THash/s despite daily fluctuations. See for example, profitability charts on bitinfocharts.com.

But all this is about to change when BSV’s fee percentage quickly rises above BTC’s, and the difference becomes bigger and bigger. See further discussions below.

In other words, the Bitcoin subsidy portions of the block rewards always cancel out with each other when compared between BTC and BSV, and as a result, any competitive difference in profitability comes only from the difference in transaction fees.

This is very counterintuitive, because one’s mind tends to gravitate toward this question: how can that be when BTC price is 300 times that of BSV?

The key: the actual prices of BTC and BSV are irrelevant in this analysis, as the dynamics is determined by the relative ratios, and the fundamental profitability is the per-unit hash power profitability (rather than the total hash power).

Now, if BSV’s fee percentage and BTC’s fee percentage were also the same (in other words, BSV-BTC fee percentage difference is zero), the transaction fee part of the economics would also be the same on BSV as it was on BTC, making the per-unit hash power profitability on both blockchains entirely equal to each other.

But as the chart shows, BSV’s fee percentage and BTC’s fee percentage are not the same.

And if you understand the designs of BSV and BTC, you will see that the difference is destined to be large. See further discussions below.

And that, is where the real dynamics lies.

BSV’s fee percentage (transaction fee/mining reward ratio) has surpassed that of BTC on July 16, 2021, for the first time, and seems to be opening up a runaway gap, standing at 4x over BTC as of August 1, 2021.

Why does this matter?

Well, it does not at this point yet, but it is going to, and it is going to matter a lot.

When the fee percentages of both blockchain are small, miners can ignore them. For example, when BSV’s fee percentage is at 4%, it is still almost negligible, despite being four times greater than BTC’s 1%, and the difference (4% -1% =3%) between the two is also almost negligible.

But once the difference between fee percentages of BSV and BTC becomes large, let’s say over 10% or 15%, it would be very hard to ignore. And a difference of 25% or greater may be impossible to ignore.

Consider a situation where BSV’s fee percentage is at 50% while BTC’s is at 1%. This would mean that on BSV, the transaction fee is the same as the block subsidy (a 50–50 split), but on BTC it is negligible. Together this would translate to a 2x in revenue per-unit hash power on BSV as compared to BTC, and profits many times higher (see below Section “What about profitability?).

The revenues in the above scenario are as follows:

- total BTC block reward = 6.25 BTC

- total BSV block reward = 6.25 BSV + 6.25 BSV = 12.5 BSV

That is, the mining revenue with a given amount of hash power would double (2x) if it is done on BSV blockchain rather than on BTC blockchain.

Similarly, if BSV’s fee percentage becomes 90%, while BTC’s fee percentage remains 1%, the total block rewards would be as follows:

- total BTC block reward = 6.25 BTC

- total BSV block reward = 6.25 BSV + 56.25 BSV = 62.5 BSV

That is, mining revenue on BSV blockchain would be 10 times (10x) the mining revenue on BTC blockchain for the same amount of hashing power.

If BSV’s fee percentage becomes 99%, mining revenue on BSV would be 100 times (100x). And so on.

Above calculations are based on ratios, and the actual prices of BTC and BSV are only relevant to the extent that they are a part of the ratio calculations.

But as said above, in reality the above scenarios are not going to happen, as miners would have moved over to BSV long ago.

For profitability and coin price scenarios that are more likely to happen, see the below sections “But what about the profitability?” and “Hypothetical scenarios” of this article.

Coin price difference and revenue comparability

Now I hear the protest: But you are comparing BSV coins with BTC coins! A reward in BSV coins is not the same as a reward in BTC coins, as BTC is presently almost 300 times more valuable than BSV per coin.

The answer is, for miners, the fundamental metrics is revenue and profitability per-unit hash power.

Provided that BSV/BTC hash ratio and BSV/BTC price ratio are the same, which has been the case historically, revenue and profitability on BSV chain measured in BSV coins would be equivalent to revenue and profitability on BTC chain measured in BTC coins.

It is straightforward math.

Only the difference in transaction processing revenues will contribute to profitability in competitive terms.

But what about the profitability?

The above discussion is based on revenues. But what about the profitability? If the cost also increases by the same proportion, there would be no change in profitability even if the revenue increases.

This is the part that is widely misunderstood or not understood at all:

In terms of energy consumption, Bitcoin’s transaction processing will be computationally far more efficient than hashing, probably by orders of magnitude.

The reason is twofold.

First, hashing competition is never about efficiency, but only about sheer power. Although the makers of hashing hardware compete on energy efficiency, at the miner level roughly everyone is on the same footing. Of course, miners all seek for cheapest energy sources, but this does not have intrinsic technological innovation for the miners themselves, nor does it differentiate between different Bitcoin blockchains, BTC or BSV.

Therefore, this part of the business stands alone on its own basis, but really cannot face any competition in the efficiency department. And the fact that it has never had any obvious competition in the past has given people a misimpression that competition does not exist and there is none to come.

Second, the transaction processing on BSV is becoming a highly competitive business and is driving a tremendous amount of technological and business innovations that improve efficiency continuously. This is how progress is made, and also how new values are created.

At the current stage when the block sizes are still not too large, the transaction processing happens almost as a byproduct, requiring almost negligible energy consumption besides the hashing itself.

This has a dramatic effect on profitability, making the profitability boost even greater than the revenue boost in the scenarios discussed above.

For simplicity, consider the following scenario (all numbers on per-unit hash power basis):

- BTC mining revenue: 100 (unit does not matter)

- BTC mining profit: 10

- Extra revenue by moving to BSV: 100

- Extra cost for mining on BSV: 0

- Extra profit for mining on BSV: 100

- Total revenue after moving to BSV: 200

Profit after moving to BSV: 110 (=10 + 100), a 11x boost from 10%.

That is, in this scenario, moving to BSV results in doubling (2x) the total revenue, and an 11x in profit. For most businesses, 2x in revenue and 2x in profit would be an expansion that is too good to resist, let alone a 11x in profit while doubling the revenue.

If we tweak the numbers toward being less favorable to BSV, we may have:

- BTC mining revenue: 100 (unit does not matter)

- BTC mining profit: 20

- Extra revenue by moving to BSV: 100

- Extra cost for mining on BSV: 40

- Extra profit for mining on BSV: 60

- Total revenue after moving to BSV: 200

Profit after moving to BSV: 80 (20+60), a 4x boost from 20.

That is, even assuming a higher profit margin in BTC mining, and also assuming mining on BSV has a 40% extra cost for transaction processing, moving to BSV results in doubling (2x) the total revenue, and a 4x in profit.

The above scenarios are only when BSV fee percentage is 50% (i.e., fee revenue counts for 50% of the total block reward). When the BSV fee percentage rises, the changes in profits are even more drastic.

For example, when BSV fee percentage is 90%, we would have the following:

- BTC mining revenue: 100 (unit does not matter)

- BTC mining profit: 10

- Extra revenue by moving to BSV: 900

- Extra cost for mining on BSV: 400

- Extra profit for mining on BSV: 500

- Total revenue after moving to BSV: 1000

Profit after moving to BSV: 510 (= 10 + 500), a 51x boost from 10.

This result assumes 40% cost in BSV transaction processing (400 units of extra cost on BSV in order to generate 1000 units of transaction fees).

Judging from the energy efficiency of the current BSV nodes, the costs due to energy consumption in transaction processing are almost negligible compared to hashing, so the 40% cost in BSV transaction processing is for covering other business overhead, not for energy consumption. This also shows how energy efficient BSV would become when compared to BTC.

Admittedly, as block sizes increase, the costs of processing and storing such blocks will also increase.

At the same time, nodes on BSV may become so sophisticated that becoming a successful BSV node is no longer a simple matter of having a sheer amount of hash power but requires special business knowledge and specialties. This would create a further barrier for a miner moving to BSV.

However, as said above, wherever there are more profits to be made, the capital and resources will figure out a way to follow. It is simple economics and capitalism.

So overall, as long as the BSV adoption continues, the mining business will all gravitate toward BSV.

Hashing difficulty level and network security

Alternatively, BTC might be forced to lower the hashing difficulty level to artificially maintain a higher price/hash ratio and make mining on BTC more profitable to prevent miners from leaving for BSV.

But to that, BSV would have the option to respond with an array of strategies it deems effective, ranging from one extreme of always matching BTC’s price/hash ratio (as it has done in the past) to another extreme of completely ignoring BTC’s move and thus breaking the current coupling between BTC/BSV price ratio and BTC/BSV hash ratio, or anything in between with a more balanced and sophisticated strategy.

Once the coupling between BTC/BSV price ratio and BTC/BSV hash ratio is broken, BTC and BSV mining would be essentially two different kinds of economies. To the extent that more hashing power is required on BSV to generate a coin subsidy having the same dollar value, BSV would have developed a different dimension of network security which BTC cannot reach, because hashing on BSV would then be objectively “harder” than that on BTC on a per subsidy dollar basis.

But to the extent that BSV miners are still more profitable than BTC miners thanks to the much higher network fee (which has much left even after compensating the deficit of coin subsidy on BSV compared to BTC), it would demonstrate itself as simply a better technology as well as a better economy.

At the same time, as the block subsidy continues to diminish through future halvings anyway, it would be beyond any doubt which technology and economy is sunsetting, and which is rising.

To the extent that mining on BSV is “harder,” however, the level of pressure for BTC miners to move to BSV may be somewhat alleviated. So there may be a curved dynamics.

The dynamics of mining

Although the above explanation involves various ratios and percentages, it really is not complex. It is simple math.

When the above-described dynamics kicks in, the only thing that could counter the avalanche effect is a divergence of the hash power ratio and the price ratio between BSV and BTC.

If you follow the above analysis, you will see that the only thing that would mitigate the pressure for miners to move to BSV is that somehow the price ratio between BTC and BSV is greater than the hash power ratio between BTC and BSV.

That is, to reduce the pressure of miner migration from BTC to BSV, the market would have to deem BTC’s hashing to be qualitatively (not just quantitatively) more valuable than BSV’s.

But how can that be? Even under the current market condition that is completely biased against BSV, the market considers BTC’s hashing to be qualitatively the same as that of BSV’s (although the market does give BTC a quantitative advantage of almost 300/1 to BSV), why would it change when BSV is clearly winning the business?

I would expect the hash ratio and the price ratio to be the same for quite long time in the future. And as illustrated above, that would be an extremely favorable condition for BSV, because the extra transaction fees would be a source of increasingly greater extra profit for BSV miners, and that would trigger an avalanche of miner migration to BSV.

But eventually I expect a curve to emerge to partially cancel the migration pressure/attraction, because an unmitigated avalanche like that is probably unrealistic.

Nevertheless, as long as the mass adoption of BSV occurs, the tectonic shift is unavoidable. It will not be a matter of personal opinions, but objective economics.

The dynamics of mining has a simple and clear signal here. The only way for BTC to avoid an onslaught/avalanche type of collapse is that BSV perpetually fails to see app/user adoption. It is quite clear that without utility, BSV would be competing against BTC as an inferior store of value, with respect to which the market has spoken. Therefore, the apps and transactions are absolutely the key.

The effect of rising BSV price on BSV’s low fee advantage—hypothetical scenarios

Some may ask: While the BSV’s fee percentage continues to go up, how does BSV’s coin price come into play? If one expects the coin price to also increase, would it not also make BSV transaction fees continue to rise and gradually lose the low fee competitive advantage?

An alternative way to put this question is: If the BSV blockchain’s competitive edge is premised on its low fees, does it even have room to allow the BSV coin price to increase?

This is a valid question, especially considering that BTC’s transaction fee, although extremely high at the present time, does not depend on the coin price and does not have to go up with the coin price, whereas BSV charges a certain number of satoshis per byte of data, and therefore the continuous rising of BSV coin price would eventually make the fee per transaction increasingly too high.

It is reasonable to assume that customers would measure fees in dollar amounts (or any other fiat preferred by the customers) even though miners price them in satoshis.

However, the above concern causes no difficulty to BSV. As the BSV coin price increases, BSV miners always have the option to lower the number of satoshis charged for per byte, to maintain the fee competitiveness.

But this raises another question: if the transaction fee in satoshis continues to drop, how can BSV maintain its higher fee percentage relative to BTC (which is the cause of pressure or attraction to BTC miners)?

As will be shown in the following scenarios, as the transaction volume increases, BSV has a lot of room to maneuver and would be able to increase the overall transaction fee percentage while decreasing the fee per transaction in satoshis.

The following is a series of hypothetical scenarios in which BSV’s fee per transaction decreases about 3x every time when BSV’s transaction volume increases 10x, still resulting in a total transaction fee increase of 3.3x.

Note the fees and subsidies are measured in satoshis, the coin price is irrelevant, as far as the fee percentages are concerned.

the present state:

transaction fee = 4; total block subsidy = 96 (unit does not matter); fee percentage = 4/(4+96) = 4%

future state 1:

transaction volume goes up 10x, total transaction fee goes up 3.3x (because fee per transaction drops by 3x), while block subsidy remains the same (in satoshis regardless of the coin price).

transaction fee = 4×3.3 = 13.2; block subsidy = 96; fee percentage = 13.2/(13.2+96) = 12%

future state 2:

transaction volume goes up 100x, total transaction fee goes up 10x (because fee per transaction drops by 10x), while block subsidy remains the same (in satoshis regardless of the coin price).

transaction fee = 4×10=40; block subsidy = 96; fee percentage = 40/(96+40) = 30%

future state 3:

transaction volume goes up 1,000x, total transaction fee goes up 33x (because fee per transaction drops by 30x), while block subsidy drops 2x (due to the next halving).

transaction fee = 4×33=132; block subsidy = 96×0.5 = 48; fee percentage = 132/(132+48) = 73%.

future state 4:

transaction volume goes up 10,000x, total transaction fee goes up 100x (because fee per transaction drops by 100x), while block subsidy drops 2x (due to the next halving).

transaction fee = 4×100=400; block subsidy = 96×0.5 = 48; fee percentage = 400/(400+48) = 90%.

future state 5,

transaction volume goes up 100,000x, total transaction fee goes up 330x (because fee per transaction drops by 300x), while block subsidy drops 4x (due to the next two halvings).

transaction fee = 4×330=1,320; block subsidy = 96×0.25 = 24; fee percentage = 1,320/(1,320+24) = 98%.

In the above scenarios, BSV’s fee percentage sequentially rises above 10%, 30%, 70%, 90% and 98%, despite that the fee per transaction measured in satoshis continues to decrease by 3x, 10x, 30x, 100x, and 300x.

Once BSV’s fee percentage rises above 30%, the difference will be substantial and the pressure will be clearly felt by BTC miners. When the BSV’s fee percentage rises to 70%, 90% and 98%, the pressure would multiply.

Once BSV’s fee percentage is about 50%, there is no way that BTC could catch up, and BTC will either collapse or have to concede that its mining economics is inferior to that of BSV and find a “political” solution to make up its market inferiority.

At the same time, the fact that in the above scenarios the per transaction fee measured in satoshis continues to drop will have profound impact on the market and price.

For one thing, this gives room for the BSV coin price to rise without affecting the per transaction fees in actual dollar amounts. That is, even with the BSV price increasing by large multiples, the fee percentage on BSV can continue to increase without affecting the BSV’s low fee competitiveness.

In other words, being able to create an unbounded economy enables BSV to maintain competitiveness in all following three areas simultaneously:

(1) competitive in the mining business by maintaining a high fee percentage;

(2) competitive in user adoption by maintaining low fees per transaction;

(3) competitive in the coin price market by providing economic grounds for price appreciation.

BTC restricted in this competition

The higher BSV’s fee percentage is comparative to BTC’s, the higher the pressure is for BTC miners to move over to BSV. This is the conclusion from the previous analysis, which assumes that the hash ratio and the price ratio continue to be the same or comparable between BTC and BSV (regardless of the actual price difference of the two coins), as they have been historically.

A 15% or higher difference between BSV’s fee percentage and BTC’s fee percentage would be hard to ignore.

For example, if BSV’s fee percentage is 25%, it would be very hard for BTC’s fee percentage to be below 10% because otherwise the fee difference would be higher than 15% (25% -10%); if BSV’s fee percentage is 50%, then it would be very hard for BTC’s fee percentage to be below 35%; and so on. (BTC’s fee percentage presently stands at 1%, but historically varied from 1% to 30%, and the fee percentage goes up when BTC price goes down and/or the number of transactions increases.)

BTC is restricted in these competing dynamics because it has no effective tools to counter. Can it increase its own fee percentage to match that of BSV? Mathematically, it can, but in practice that would be committing suicide, because the only ways for BTC to do that are (1) reducing the hash power (but accordingly reducing the BTC price); or (2) increasing the fee per transaction. It clearly cannot continue to do any of that without collapsing the blockchain.

One might still ask at this point, why can’t BTC increase its profitability simply by the virtue of perpetually increasing BTC price?

Well, the fact that it cannot be done is the point of this article.

First off, even if the competitive dynamics brought in by BSV did not exist, it would still be mathematically infeasible to expect the BTC price to go up perpetually. But that is not even what matters here. It is the competitive dynamics brought in by BSV’s network fees that matters. A higher BTC price means higher hash power, but the higher hash power is not going to come because the hash power would be attracted to BSV to make more money due to the surplus profit from the higher network fees on BSV. This is because, as analyzed above, BTC block reward per-unit hash power (unit profitability) cannot surpass that of BSV, which in turn is because the mining subsidy per-unit hash power is always evened out by the same on BSV, and the only difference comes from the network fees, which is increasingly higher on BSV.

So BTC is inherently restricted, and things cannot happen freely on BTC’s terms. Everything is going to be framed and driven by the increasing BSV network fees, and BTC will be forced to become a lame-duck as far as the competition for miners’ processing power is concerned.

Another perspective from block size

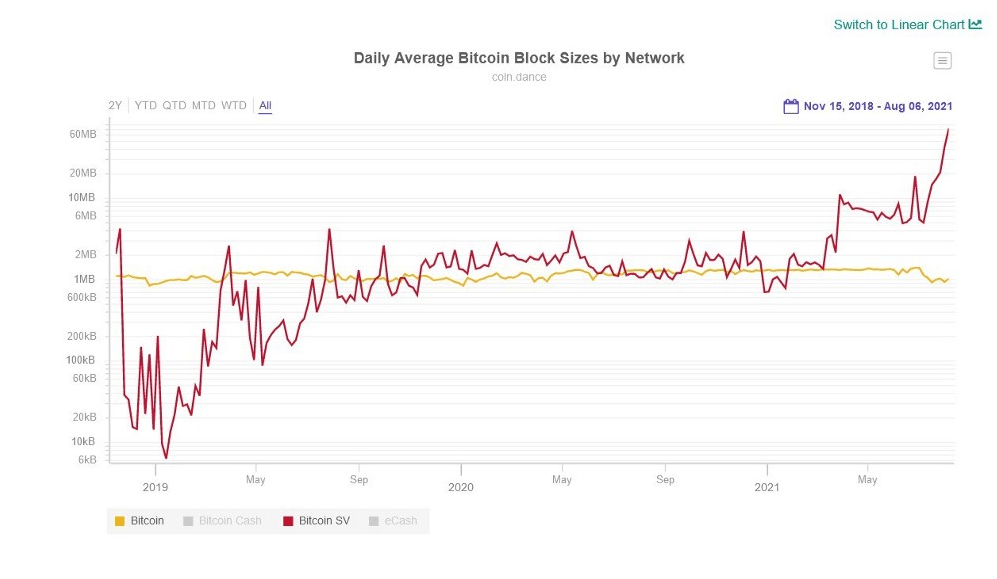

Because BSV nodes charge fees per byte, the clearest indication of the pressure created by BSV is the average block sizes.

As the chart below shows, BSV’s average block size started very small in 2019, rose to a level comparable to that of BTC during 2020, but took off in early March 2021, and started to rise exponentially, currently standing at about 50 times that of BTC (50MB).

Note the chart is logarithmic because the BSV growth is exponential.

The larger the BSV block size is, the higher the pressure is for BTC to keep up. And once BTC price fails to go high enough to keep its hash power, the downward spiral starts, due to the pressure created by BSV. As long as the BSV block size keeps increasing, the pressure increases.

And the pressure on BTC miners would create a vicious cycle. First, hash power is being attracted to BSV due to apparently higher profitability per-unit hash power, diminishing the actual and perceived quality of the BTC network, thus creating downward pressure on BTC price. But this is a death spiral, because once the BTC price goes down, mining on BTC becomes further less profitable compared to that on BSV, so the vicious cycle continues.

The BSV’s average block size is currently about 50MB, 50 times that of BTC and grows exponentially. Yet people are not paying attention to it, must be because BSV’s total transaction fee per block in dollar amount is still about 100 times smaller than that of BTC.

But people will notice it when miners finally do. If they don’t notice it when the BSV’s average block size is 50 times that of BTC, perhaps they will do when it reaches 500 times? They should notice it much earlier if they are smart, as the growth trajectory is exponential.

Regardless of the attention received, BSV’s average block size will continue to go up on a projected track like this: 1(MB) > 5 > 50 > 500 > 5,000 (5GB) > 50,000 > 500,000 > 5,000,000 (5TB)…

A critical point on the way to reach the BSV BTC parity:

In particular, note that when BSV’s average block size reaches 5GB (a further 100 times increase from the present 50MB level), the BSV block transaction fee may reach same order of magnitude with BTC’s transaction fee on absolute terms (or in actual dollar amounts), not just on relative terms (or in each chain’s respective satoshis).

To do this estimation, let’s first assume that BSV/BTC price ratio remains 1/300 (unlikely true, see below). At block size 5GB, and fee 0.5 sat per byte, the total fee for one block would be 2.5B satoshis, or 25 BSV.

For simplicity, we assume in the discussion below it is before the next halving unless noted otherwise. (If this happens after the next halving, the comparison would be progressively more favorable to BSV, because the network fees are not affected by halving.)

In this case, BSV’s total block reward is 31.5 BSV (25 + 6.25) versus BTC’s 6.25 BTC (the present block subsidy), with BTC’s fee at a negligible percentage. Because BSV/BTC price ratio is assumed to be 1/300, BSV’s total block reward would be about 0.105 BTC versus BTC’s 6.25 BTC. BSV is much smaller.

However, the BSV’s network fee is at the same scale as BTC’s network fees, which is currently only about 0.1 BTC (and remember BTC’s fee is fundamentally limited and does not go up like BSV’s does). If you don’t immediately realize how this would be absurd, remember BTC miners generate this same amount of fees using 300 times as much hash power.

Therefore, with BTC/BSV hash power ratio at 1/300, a miner moving a certain amount of hash power to BSV would generate network fees hundreds of times that on BTC with the same amount of hash power (assuming the other costs are relatively small), on top of the block subsidy leveled on a per-unit hash power basis. The pressure for BTC miners to move is clearly tremendous.

Therefore, it should be economically obvious that BSV/BTC price ratio and BSV/BTC hash ratio cannot still remain 1/300 when BSV’s network fees increases a 100x while BTC’s remains the same.

This is because, if that were the case, by that time, on a per unit cash power basis, mining on BSV would be ridiculously more profitable than on BTC.

That is, it would be economically absurd if the BTC/BSV hash power ratio, and accordingly BTC/BSV price ratio as well, remain 300, or even 30 times for that matter.

What is reasonable at that point can only be: even if BSV’s hash power (and price) may still be somewhat smaller than BTC’s, it would have to be within the same order of magnitude (a difference of a few times at most).

What if the BTC/BSV hash power ratio and thus BTC/BSV price ratio are reduced to 30 rather than 300, will the economics become reasonable?

At this price ratio, BSV’s total block reward would be about 1.1 BTC versus BTC’s 6.25 BTC, much closer but still smaller but on the same orders of magnitude.

You may ask, BTC/BSV price ratio at 30, is that realistic?

First, it is within the range of this ratio once had been, therefore not outlandish even just considering the history, much less considering a future where BSV’s block size has increased 100 times.

Second, it is not plausible that BSV price will remain the same when its average block size has been increased by 100 times.

It would make much more sense if we take the above-described future state 2, in which BSV’s transaction fee goes up 100 times from the present level, and BSV price goes up 15 times. Now, even if BTC’s price itself is also 50% higher than its present level by that time, BTC/BSV price ratio would be at 30 instead of 300.

And this is when miners would have been under continuous increasing pressure to move from BTC to BSV for quite some time. It would be highly questionable to assume that BTC price will still be 50% higher than its present level. That is simply too favorable an assumption about the price of BTC.

After this price ratio adjustment, if BSV’s fee per transaction charge in satoshis does not change, the economics would remain unbalanced on the unit-hash power basis, in favors of BSV, because the BSV now uses 1/30 of hashing power to generate total fees that are 10 times that of the BTC fees, still having the 1/300 overall disparity in energy efficiency, even though BSV mining is still a smaller economy measured in total size at this point.

Now, what if BTC/BSV price ratio is further reduced to 5 by then?

BSV’s total block reward would be about 6.3 BTC versus BTC’s 6.25 BTC (or 6.25 BTC versus 3.125 BTC if it is after the next halving), now at simple parity or beyond.

Note that here we are talking about total block reward in absolute terms (both in BTC coins which can be translated to dollar amounts on a single basis, rather than in each chain’s respective satoshis). That is, it is no longer merely about per-unit hash power competitiveness, but the entire scale of the economy on absolute terms.

If you had thought that BTC/BSV price ratio being reduced to 5 was impossible, now think about the above numbers, you should see that even then the economics still favors BSV significantly, because you see two economies use disparate amounts of energy (a 5x difference), but generate outputs that are on the same scale.

In reality, the results would be more complex than the above examples because BSV will likely lower the per transaction fee when BSV price rises, requiring adjustments in the above estimates. Whether and how much BSV will (or need to) lower the per transaction fee will depend on the actual BSV price at any time. But overall, the economics will be always in favor to BSV, by virtue of its constantly creating a larger economic space, while BTC is more and more restricted (see the above Section “The effect of rising BSV price on BSV’s low fee advantage — hypothetical scenarios”).

Admittedly, by then, the costs for processing big blocks would be significant and must be counted in the calculations. But even if the cost for processing the blocks at the time is four times (4x) that of the hashing cost, we would have two systems at parity in terms of the efficiency.

It is also possible that, by then, the coupling between BTC/BSV price ratio and BTC/BSV hash power ratio would have been broken, in order to carve out some extra room for BTC to survive. But as said, the decoupling would make BSV’s network security qualitatively better than BTC, besides all the other economic advantages.

5GB block size is therefore a critical point on the way to reach the BSV BTC parity.

And once BSV’s average block size reaches the above-mentioned critical point (5,000 times that of BTC, or roughly at 5GB per block), there is no stopping for it to go even higher. BSV’s Teranode architecture aims at block sizes above 1TB.

In addition, at that point, another dynamic factor would have come into play: BSV would have a tremendous amount of room to further reduce fees while still maintaining superior miner profitability.

Lower and lower fees are catalyst to an explosive further mass adoption.

How far is BSV away from reaching the above critical point, where the present average block size has been increased by 100 times?

It depends on the adoption. But remember, once adoption starts, it is exponential.

For example, if it doubles every month, it takes less than 7 months to reach 100x. If it doubles every three months, it will take about 20 months to reach 100x. But if it doubles every half year, it would take a little bit over 3.5 years to reach 100x.

For reference, during July 2021, BSV’s average block size went from 7.7MB to 46MB, about a 6x growth. Even if the data of the several days of the largest jumps are taken away, the growth speed in the last month was at least 4x, which is essentially doubling every two weeks, and at such a speed it would reach 100x in less than 4 months.

It is therefore reasonable to project BSV reaching 100x average block size (5GB) within the next year or two.

If you do not understand the above statements, please re-read this article.

Summary:

Note that I am not doing a chart-based technical analysis. What I did in this article was a far more fundamental economic analysis.

Once you understand the intrinsicality in the chart and the above analysis, you will see it is checkmate to BTC.

I’m not saying that the particular outcome is unconditionally guaranteed. All I’m saying is that if the BSV average block size keeps going up, the outcome is guaranteed.

Killing BTC is not the goal of BSV. It is still possible for both to be successful in serving their different purposes. However, based on the trend analysis above, the kind of expansion that BSV is going to have is intrinsically restrictive to BTC due to natural competitive economic forces. BTC therefore faces growing pressure as BSV grows, even if there is no intentional competition.

Even if BSV itself grows as expected, it will not reach success without some very serious fights, including fighting against malicious and illegal attacks. For some parties, there may be simply too much at stake due to the strange history of Bitcoin, and therefore may act not according to the normal incentives of the next block mining but rather some other nefarious motives.

In addition, the economic analysis is premised on the rationality of actors, but there are many irrational actors in the world.

However, if the dynamics is strong enough, ultimately the economic reality takes place against the backdrop of illegal attacks and irrational acts.

Finally, it is a perilous thing to make a theoretical prediction. Most people are probably even not interested in hearing such predictions, but rather hear about things that have already happened. Many cannot tell the difference between a speculation and a theoretical prediction, but blessed are those who do, as that is the difference between astrology and physics. Personally, it may be easy to withhold speculations, but not easy to withhold a theoretical prediction which I have become highly confident of.

So here it is, my theory, stands to be tested.

PS Notes, Q&A:

1. But miners also consider other factors such as speculating and cashing out, how will that play into the economics?

These factors are real. But it’ll all change dynamically and would easily shift in favor of another chain when the price and profitability shift. It may be impossible to predict an exact time point when certain change may occur, but the overall trend is pretty clear. People who have done mining will not only understand this but can actually feel it when the time comes.

That’s why the ultimate “argument” for BSV is the real numbers that reflect an economic reality. The numbers have just started to emerge since last month. Prior to that, there was a lot of great theories and solid reasoning, but it was too much foresight for most people.

That’s also why I try not to blame the market, not even the digital currency market, for its stupidity, although it’s full of that. Even the stock market, as speculative as it may be, has real numbers, such as P/E ratios, to at least give people a psychological guide. Digital currency market has none now. It’s pure speculations. In fact, it is the worst kind of speculations, because some speculations (e.g., stock market) can be based on some reasoning and knowledge, while digital currency market speculations at the current stage are almost completely a publicity vote by a blind mass’ enthusiasm driven by a lack of information or misinformation.

But BSV will produce real economic numbers, entrepreneurs will feel that first, smart investors will then follow, and then finally the mass. This is the right order.

Presently, the order is reversed in the digital currency market. The cart is placed before the horse, but the cart is flying due to people’s imaginations and the blind following the blind.

2. What is the evidence to support that big block size correlates to economic success?

This is the central point I tried to make in this article. I did not assume this, but rather provided evidence to prove it is the case.

I know where this question comes from, because prior to this I had always thought the same way, like:

“It is nice and well, even looking promising, to have big blocks, but you can’t simply assume that big blocks mean better node (mining) economics, especially when compared to BTC which has led to a large successful mining industry.”

But then I came to this realization: the way BSV nodes are designed to operate, big blocks translate straight to not only higher fees but also an increasingly greater extra profits relative to BTC. Therefore, once the difference between BSV’s fees and BTC’s fees becomes obvious and hard to avoid economically, miners will be pressured to switch to BSV.

And the above in turn is because the bitcoin subsidy portions of the block rewards always cancel out with each other when compared between BTC and BSV.

The above last point is something that is very counterintuitive, because one’s mind tends to gravitate toward this question: how can that be when BTC price is 300 times that of BSV? But the key is: the actual prices of BTC and BSV are irrelevant in this analysis, as the dynamics is determined by the relative ratios, and profitability is most fundamentally that per-unit hash power (rather than the total hash power).

I must admit that I never thought about this clearly until just a few days ago. I did a lot of explaining in the article why this is the case. I hope at least some people would give it a serious read and think about it.

3. When will this happen to affect the prices?

Because of the dynamics discussed in the article, one can objectively say that the temporary price of BSV does not matter, AS LONG AS apps, users, and summarily average block sizes, keep going up. This is explained in detail in the updated article.

The analysis in the article, however, is conditional: it is only effective when the difference between BSV’s fee percentage (of the total block reward) and BTC’s fee percentage is appreciable (say at least 15%). Currently, the difference is about 3–4%, but rapidly rising.

I really would like to see what happens when BSV’s fee percentage reaches 50% or higher, because it would create an impossible situation for BTC. Once BSV’s fee percentage reaches 50%, the difference between BSV’s fee percentage and BTC’s fee percentage will be at least 15% (50%-35%), and up to 49% (50% -1%), reaching a range of margins that are impossible to ignore by rational miners.

This 50% point would have been reached when BSV’s average block size reaches 1.25GB, well before the 5GB critical point discussed in this article, in which the BSV fee percentage would be close to 80% (or close to 90% if happens after the next halving).

According to the historical data, BTC’s fee percentage itself can vary from 1%-35%. However, it is a generous estimate for BTC, because the historically higher BTC fee percentages were all due to the following conditions: (1) the BTC price was low or suddenly went down dramatically; (2) and at the same time transactions still reached the maximum both in terms of the volume and the fee per transaction. This a rather odd condition, and only transitory even if it happens. In the history of BTC, the average fee percentage during longer periods has always been kept under 10%.

More importantly, because the BTC transaction fee has already reached the maximum level that users and the market can tolerate, BTC’s only hope for a greater fee percentage is, undesirably, a lower BTC price. For example, if BTC price goes down by 90% of the current price (a 10x drop), the BTC fee percentage would rise from the current 1.5% to 13% (not 15% due to percentage math), but still much lower than the historical high of 35%. And if BTC price goes down by 99% of the current price (a 100x drop), the BTC fee percentage would rise from the current 1.5% to over 50% assuming that at the time BTC can still charge a fee per transaction as high as today’s. But that’s extremely unlikely, because the only reason why users can tolerate BTC’s extraordinarily high transaction fee is because (1) high price of BTC coin; and (2) speculations of even higher price in the future. When BTC price crashes, so will the transaction fee.

In contrast, BSV’s fee percentage can potentially go as high as 99% and continue to stay there. The difference is not only quantitative but also qualitative, because with BTC, due to its restrictive nature, the occurrence of an unusually high fee percentage is almost always a bad signal, while with BSV, even with a fee percentage as high as 99%, there still will be room for positive coin price actions, because its unbounded space sets out a synergistic economy that grows larger and larger, rather than a rent-seeking zero-sum game as with BTC.

4. Why would BTC miners moved to BSV, instead of much larger digital currency such as Ethereum?

Miners are less ideology-driven and more profit-driven in general. However, to the extent that the forces behind BTC control some of the miners, it is not going to be a smooth transition. Therefore, whether BTC miners will move to BSV or Ethereum is not going to be a clean picture.

But because of the following reasons, BSV will receive a disproportionately large portion of the BTC mining exit.

(1) If BTC mining starts to show signs of weakness due to the rising profitability of BSV mining, miners that decide to move would have a clear understanding what is causing it, and that would be BSV specifically. So the natural choice is firstly moving to BSV. Some may go to other blockchain such as Ethereum due to various reasons, but BSV is a natural destination.

(2) BSV’s rising mining profitability cannot happen in abstract, but has to be based on certain concrete reasons, which are almost certainly to be BSV’s success in real applications such as esports, tokenization, and smart contracts. This means that BSV in that case would not only be beating BTC, but clearly threatening Ethereum and other competing blockchains as well. This would give a further reason for miners to move to BSV instead of Ethereum. If BSV find success in more esoteric applications such as fractal database, decentralized data, decentralized computation, and decentralized AI, more power to BSV, because it would put BSV in an unrivaled position.

5. Are there any hard rules in place that are preventing BTC from also increasing the block size limit?

No, there is no hard rule that BTC cannot adopt big blocks as well. But they won’t, at least not until they see the writing on the wall. For reasons why, you need to understand the history of BTC and what has formed a foundation of their narrative. I recommend a reading: BTC and BSV, what is the real difference?

On the other hand, I would not be surprised if BTC declares a limited increase of their block size, to say 2MB or even 8MB, in the future. After all, they will have to cope with the reality.

However, once they make that move, they essentially validate what big blockers have been saying, and will also have a hard time to reconcile with their narrative. This is because 1MB was not a random number to begin with. It was carefully chosen to make sure that small personal computers can always hold the entire BTC blockchain. You might argue, because PC storage capacity is always increasing, so BTC should be able to increase its block size without destroying its narrative. But no, the total BTC blockchain size increases with time as well. So 1MB will remain its magical number.

The small block size is a meaningless goal to strive for if you see how completely useless those PC “nodes” really are, but it is nonetheless a pillar in the BTC narrative. Like many other public narratives, leveraging people’s ignorance is a powerful tool, powerful not only against the audience, but also against the owner of the narrative because it becomes an addictive condition.

But at the same time, even if BTC does make a limited compromise as indicated above, it will not stop the avalanche caused by BSV (assuming that BSV sees mass adoption).

6. Do you see an increase in smaller miners mining BSV instead of BTC?

There have been no significant moves of BTC miners to BSV so far. As analyzed in the article, at the present time, the difference in the fee percentage is just too small (less than 5%), and no one notices it. But they will eventually, perhaps when the difference is greater than 15%, 25%, or even 50%.

However, some BTC miners have always done mining on both BTC and BSV. For example, Binance’s mining division had done that for a long time until there were ordered not to. These miners do not do this because they support BSV. They engage with this “duality” simply because the profitability of mining on BTC and BSV are essentially comparable on per-unit hash power basis even when the subsidy constitutes almost all of the block reward. So even before the pressure/attraction of the BSV transaction fee economics kicks in, for smaller miners that are not bound to a certain ideology or controlled by an interest group, the question would be “Why not?”

But before miners are actually pressured to move due to the shift of economics, such duality has no significance, all because of the historical and ideological bias against BSV.

This article was lightly edited for clarity.

Watch: CoinGeek New York panel, How to Achieve Green Bitcoin: Energy Consumption & Environmental Sustainability