03-27-2026

03-27-2026

|

Getting your Trinity Audio player ready...

|

U.S. digital asset exchange Gemini repeatedly lied to its Earn account customers about being insured by the Federal Deposit Insurance Corporation (FDIC), a new report claims.

The exchange reportedly kept referring to the FDIC in its communications with clients who were worried about the safety of their funds, Axios reports. This assurance led many clients who held its interest-bearing accounts to conclude that their funds were safe and would be refunded in the case of a Gemini collapse.

Gemini halted withdrawals for 340,000 clients after the collapse of Genesis, its business partner, which filed for bankruptcy last month.

The FDIC has warned digital asset companies against making false claims regarding their insurance status. Last August, it issued cease and desist letters to five VASPs, demanding they stopped making “false and misleading statements about FDIC deposit insurance.” These companies included FTX.US, the American subsidiary of Sam Bankman-Fried’s collapsed digital asset exchange FTX.

While its peers were receiving warnings, Gemini kept on referencing the FDIC in communications with its customers, Axios reports, citing several emails from the company to frantic customers.

Gemini was, however, vague about the FDIC links. The outlet reports that most of its emails seemed to reference its deposits at outside banks rather than users’ deposits in its Earn product. In addition, it kept referring to Gemini USD (GUSD), its own stablecoin.

In one sample email to one of its clients, Gemini stated:

“GUSD reserves are held by Gemini in accounts at U.S. FDIC-insured bank accounts and money market funds holding short-term treasury bonds.”

“The cash portion of these GUSD reserves may be eligible for FDIC ‘pass-through’ insurance for Gemini customers, in the event of the failure of a bank holding the U.S. dollar deposit portion of the GUSD reserves.”

“So responding to your question, the risk of holding GUSD is minimum, and in the unlikely event of any trouble/issue, your funds remain secure.”

While customers say they couldn’t tell the distinction, legal experts believe this could be the argument that gets the exchange off the hook.

“Is it skeezy? For sure. Is it illegal? I don’t know. I can’t really say,” Todd Phillips, a former senior attorney at the FDIC, commented.

How to get away with deception

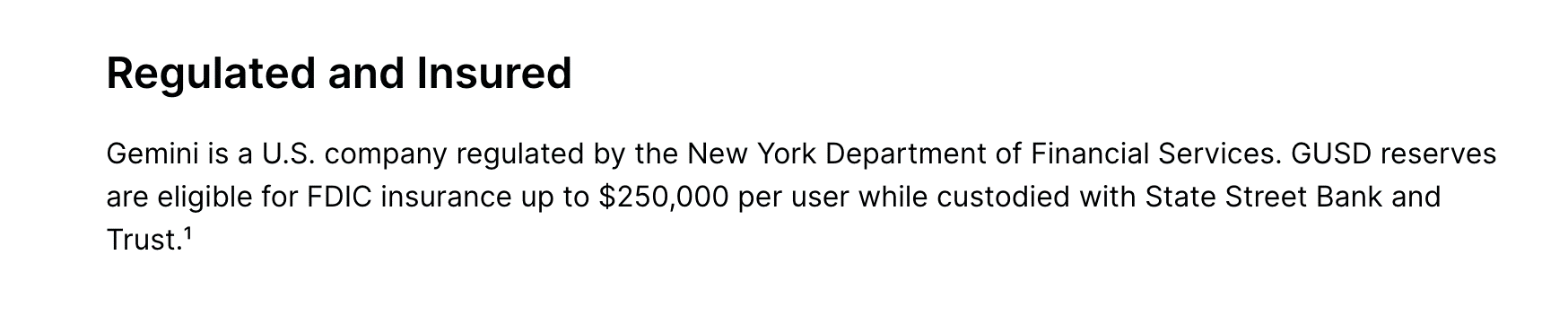

Gemini still has a portion titled “FDIC Insurance” on its website. Under this, it claims that each GUSD corresponds to one USD held as “deposits in U.S. Federal Deposit Insurance Corporation (“FDIC”)-insured banks.”

It adds that the cash portion of its reserves is held at Silvergate Bank, State Street Bank, or Signature Bank. It further claims that these funds may be eligible for ‘pass-through insurance’ if the bank holding the funds goes down.

It’s this last part that is attracting scrutiny in legal circles. Pass-through insurance refers to ‘per-user’ insurance. However, its terms of use seem to be referring to the company’s compliance with typical requirements for per-user insurance as ‘FDIC-insurance eligibility.’

This messaging, while deliberately vague, has been a constant marketing tactic for Gemini for years. The company has been throwing around FDIC in its branding as far back as 2020.

Source: Gemini

“Everybody knows the value in terms of investor comfort and confidence in something that is FDIC insured,” Dennis Kelleher, the president of Better Markets, an organization that lobbies for tighter financial regulations, said.

Kelleher added that Gemini knew what it was doing with the FDIC links. The goal was to give its users “false comfort and get legitimization” for its yield-bearing product.

Gemini is likely to get away with the deception. With its marketing materials never explicitly stating that Earn accounts were FDIC-insured, it would likely argue that the clients had a duty to understand the terms of use before depositing their funds.

Even if it breached FDIC guidelines, the agency isn’t known for being stringent in enforcing its regulations. According to legal experts, the FDIC has only conducted one enforcement in the past 15 years, and even that only resulted in a $100,000 penalty.

Follow CoinGeek’s Crypto Crime Cartel series, which delves into the stream of groups—from BitMEX to Binance, Bitcoin.com, Blockstream, ShapeShift, Coinbase, Ripple,

Ethereum, FTX and Tether—who have co-opted the digital asset revolution and turned the industry into a minefield for naïve (and even experienced) players in the market.

Recommended for you