04-12-2026

04-12-2026

|

Getting your Trinity Audio player ready...

|

It all started as a crash of a digital asset lender which promised more than it could deliver, but with each new day, the web gets bigger, sucking in more and more players and exposing new layers of rot, recklessness, and theft. Now, the bankrupt Celsius Network is countersuing an ex-manager who had sued it for operating a Ponzi scheme.

It all started in early July when Jason Stone, the founder of KeyFi, a DeFi aggregator that Celsius acquired, took to Twitter to reveal that he was the mysterious figure behind a famous Oxb1 address.

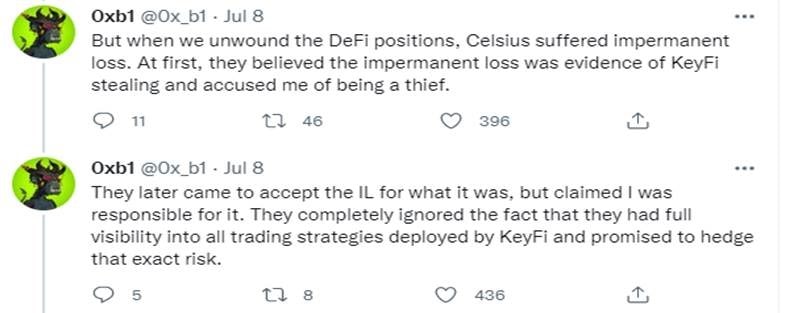

Hi all! I’m Jason Stone, and from August 2020 until April 2021, I led the group of talented individuals who managed the 0xb1 address.

— 0xb1 (@0x_b1) July 7, 2022

This address was created in August 2020 and rose to fame by giving away millions of dollars through airdrops to digital asset fans. With little information known about it, many assumed the address was controlled by a whale who was just a big philanthropist. Little did anyone know that the money that was being given belonged to investors in Celsius.

Stone sued Celsius for mismanagement of clients’ funds, claiming the lender lacked basic security and risk management systems. The lawsuit, filed in New York, further claimed that Celsius was using late-stage investors’ funds to repay earlier investors, thereby operating a Ponzi scheme.

“The recent revelation that Celsius does not have the assets on hand to meet its withdrawal obligations shows that Defendants were, in fact, operating a Ponzi-scheme,” the lawsuit reads.

Given the public speculation about the company’s solvency, and my observation of Celsius’ loose relationship with the truth, I feel it is only prudent to finally set the record straight. I have brought legal action against Celsius to settle this issue once and for all.

— 0xb1 (@0x_b1) July 7, 2022

One of the key accusations in the lawsuit that shows the extent of the rot at Celsius (if proven to be true) is a claim that CEO Alex Mashinsky used client deposits to pump the price of the CEL token. Stone claims that the lender was purchasing hundreds of millions worth of CEL tokens to give the illusion of market demand and pump its price.

This stretches as far back as February 2020, when Stone allegedly learned from Celsius’ head of coin deployment that the lender had purchased $90 million worth of CEL using customer deposits.

“The purpose of this scheme was both fraudulent and illegal […] by purposefully and artificially inflating the price of the CEL token, Celsius was able pay customers who had elected to receive their interest payments in the form of the CEL token even less of the crypto-asset,” he said.

“In addition, by artificially increasing the price of the CEL token, Mashinsky – who personally owned hundreds of millions of dollars’ worth in CEL token at its height – was able to enrich himself considerably,” Stone added.

Celsius fires back, calls ex-manager a thief

Mashinsky and his team aren’t taking the accusations lying down. Celsius has countersued Stone and KeyFi, accusing them of being inept at investing and even stealing from its clients.

Filed in New York’s bankruptcy court, the lawsuit arises from Stone’s “incompetence, deceit, and conversion, and seeks to require [him] to turn over valuable property they stole from Celsius and to pay damages and restitution for the substantial injuries the Defendants have caused through their flagrant breaches of duty.”

The lender claims Stone stole millions of dollars by buying valuable NFTs with Celsius digital assets. He also used these assets to invest in several blockchain startups where he still holds stakes wrongfully. To cover his tracks, he reportedly obfuscated the trail by using Tornado Cash, the digital assets mixer that was recently banned by U.S. authorities.

But Stone has previously claimed that he didn’t steal anything from Celsius.

The counter lawsuit against its ex-manager isn’t the only legal action Celsius has taken in the past few days. This week, the lender sued Prime Trust, a digital asset custodian, seeking to recover $17 million worth of assets.

According to the lawsuit, Prime Trust had about $119 million worth of Celsius’ assets but failed to return 398 BTC, 196,268 CEL tokens, 3,740 Ether, and 2,261,448 USDC, worth a combined $17 million. Celsius is seeking a court order compelling the custodian to turn over the assets it has allegedly refused to give back.

Prime Trust hadn’t commented on its role in the Celsius saga at press time.

Follow CoinGeek’s Crypto Crime Cartel series, which delves into the stream of groups from BitMEX to Binance, Bitcoin.com, Blockstream, ShapeShift, Coinbase, Ripple,

Ethereum, FTX and Tether—who have co-opted the digital asset revolution and turned the industry into a minefield for naïve (and even experienced) players in the market.

Recommended for you